Looking to buy a home but have bad credit?

You aren’t alone!

While having bad credit can sometimes hinder you from finding your dream home, there are ways around this problem. Keep reading for financing options as well as how to improve your credit.

What is Your Credit Score?

You need to always be aware of your credit score!

But what exactly is credit?

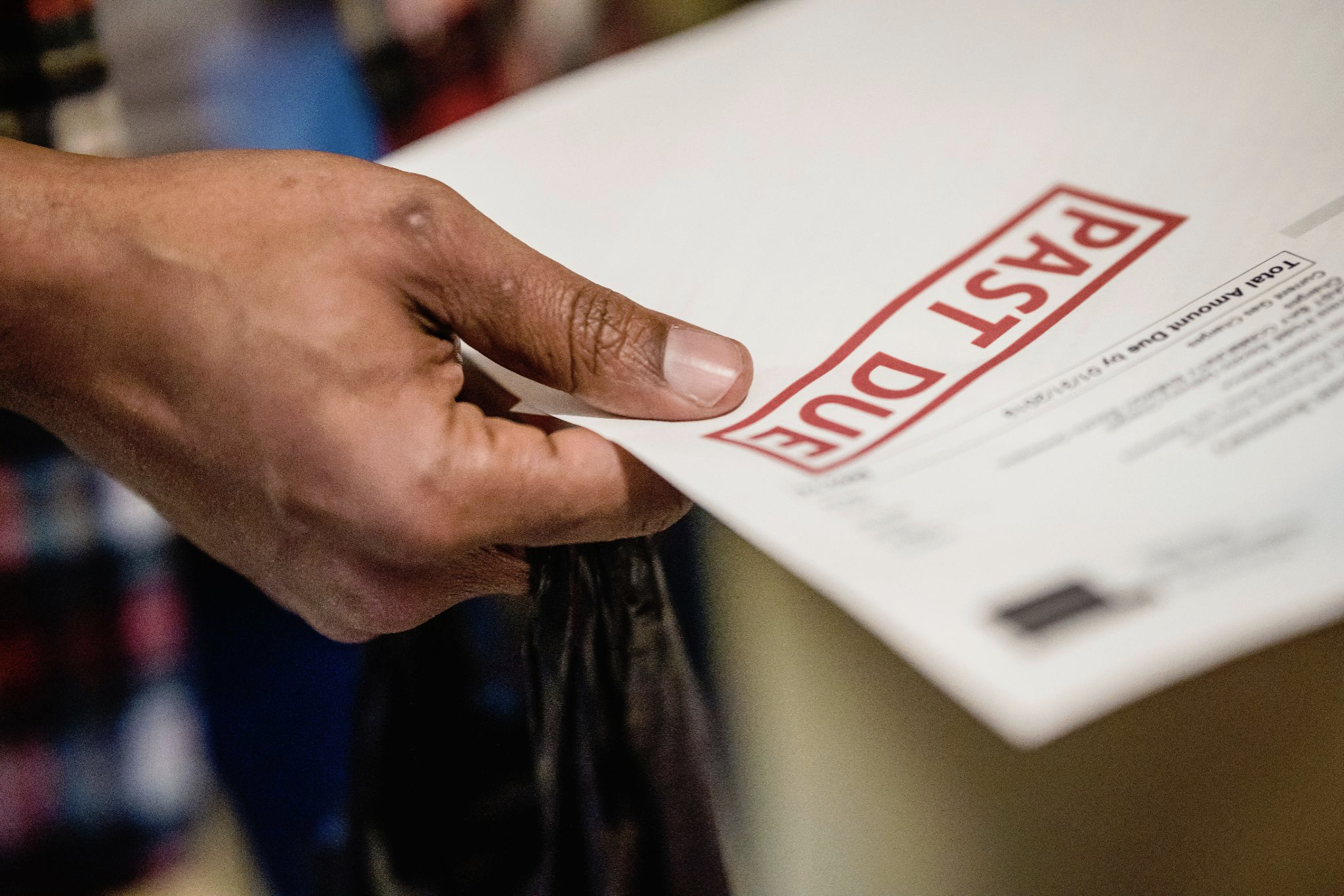

Basically, credit means you have a public record that tells businesses and money lenders whether you are likely to pay back what you borrow (and on time!).

It’s always a good idea to stay on top of your credit and pay back what you borrow when you’re supposed to. That way you will have a good record that will allow you to buy a home or a car or whatever else you may want.

Unfortunately, life gets in the way.

Whether it’s a lost job, costly healthcare, or getting into serious debt, credit can easily be affected after just one missed payment.

Whether it’s a lost job, costly healthcare, or getting into serious debt, credit can easily be affected after just one missed payment.

How can I track my credit?

There are several options to track your credit score. Some charge a monthly fee but there are also free apps that can also do the job.

What is considered “bad credit”?

While the credit scale can vary, having a score of 650+ will give you a good chance of getting a loan, while having a score of 620 or less will most likely cause problems with obtaining financing.

So, if your credit score is ≤620, and you’re looking to buy a home, what should you do?

First, Consider Your Situation:

What is your annual income?

What is your annual income?

Not only do you need to consider how much you are making, but you also have to include your debt-to-income ratio. Are you paying more in bills/debts than you’re making?

In other words, do you have more money going out than coming in?

(You can calculate your debt-to-income ratio here.)

Do you have enough money for a down payment? The more money you have to put down, the better, but aim for at least 20% of the sales price.

Loan Options

Now that you have taken the time to evaluate your situation and what you can afford, here are some options to consider.

FHA Loans

FHA (Federal Housing Administration) loans have the option of lower credit minimums and low-down payments and are recommended for first-time buyers. While there are specific requirements to meet for an FHA loan on a mobile home, this is a great option if you qualify. There is also the requirement to pay mortgage insurance.

Fannie Mae

While you do have to pay mortgage insurance with Fannie Mae, it can be canceled once the borrower reaches 20% equity. Fannie Mae has a variety of options for mobile home borrowers and offers loans to those with credit scores as low as 620.

While the repayment period is shorter than traditional loans, the APR and interest rates are higher.

Rent to Own Contracts

This is not a very common option. However, if you can do this, it will help you build your credit while giving you time to save up for a down payment.

There are several options you can choose from when signing this type of agreement. Be sure you understand all terms of the contract before you sign! Always lean on your local real estate agents and title companies for proper guidance on all contracts. There are certain items that need to be done to protect you, and your future investment.

Personal Loan from a friend or relative

This is for the people with families in good financial situations. While this may be an option for you, think carefully before jumping into this situation.

Just like any other loan, there need to be terms lined out for the borrower and the lender. No matter what, a personal relationship is worth a lot more than a home loan!

Seller financing

Also known as “in-house” financing, this can turn into a scam if you aren’t careful. Mobile home parks make it easy to finance a mobile home, but there are many traps to look out for. Beware of places that offer to carry the note and not require bank approval or that offer interest rates that seem too good to be true… because it most likely is.

Veteran Assistance Loans

If you’re a veteran, this may be the perfect option for you. These loans give veterans opportunities to buy mobile homes with a much simpler application process as well as government assistance for repayment. There are four types of VA loans that you can look into, offering loans for anything except vacant lots or co-ops.

Credit Union Financing

Financing through a credit union is generally cost-effective and provides flexibility to borrowers. These types of loans are not usually known about and have several pros, such as lower down payments and lower interest rates.

Freddie Mac

Freddie Mac has a great site that breaks down everything you need to know about obtaining a loan through them. This loan is for low to moderate-income borrowers that want a conventional loan.

Tips to improve your score

If you still are unable to secure financing for a mobile home, it’s still possible! Continue to keep working hard to build your credit and save money and you are well on the way to becoming qualified. Focus on improving your score by doing these three things:

- Stay focused on steady employment. Home lenders want to see applicants at the same place of employment for at least 2 years.

- Pay attention to your debt-to-income ratio. Keep it as low as possible (well under 50%).

- Your income must appear to continue for the next few years of applying for a loan.

If you currently reside in a rental, this may be a great time to focus on building up your credit and saving up for a down payment.

Have more questions? Give us a call at Century 21 Upchurch today!

Sonny Upchurch Cell: 972-365-5176, Office: 903-356-3116

Sonny Upchurch, October 11, 2022